Solving the Pharmacy Pricing Maze

2026-04-23 · by Jonathan McAdory, PharmD

It's unfortunate, but many of us — if not all of us — have experienced this exact encounter at some point or another. You get to the pharmacy counter and despite having paid into an insurance plan every single month, you're met with the terrible, unexpected news: your medication is much more expensive than what you had anticipated.

For patients, this may feel like the pharmacy staff secretly collaborated with your insurance company to deny your benefits, and they probably even all gathered around in the back and had a big laugh about it at your expense. But I can promise you this is not the case. I, as well as all other staff, sincerely wish every patient had affordable coverage on their medications, and it would make everyone's life ten times easier if this were the case. But unfortunately, it remains a fact of life: even with prescription coverage, patients are often stuck paying giant sums of money out of pocket. Why is that?

Why Is My Prescription So Expensive?

1. Prior Authorizations (PAs)

Prior authorizations are a frequent source of frustration for both patients and providers. While the process can feel burdensome and time-consuming — often taking several days to a week or more — these requirements serve an important purpose in the healthcare system. They help ensure that medications are used appropriately, following established clinical guidelines and step-therapy protocols, thereby protecting patient safety and controlling costs.

For example, a newly diagnosed diabetic patient may be prescribed Ozempic (semaglutide). Although this medication has gained popularity for weight management, insurance plans typically require a trial of a lower-cost, first-line option such as metformin before approving coverage for more expensive therapies. This step-therapy approach helps confirm that the higher-cost medication is medically necessary.

2. Quantity and Fill Limitations

Insurance plans often impose limits on the quantity or duration of certain medications. A common example involves proton pump inhibitors (PPIs) used to treat GERD or acid reflux, such as pantoprazole (Protonix). Plans may restrict coverage to a maximum of 90 days of therapy within a 12-month period, requiring patients to first try over-the-counter or preferred alternatives like famotidine (Pepcid).

Similar restrictions apply to dosing frequency. For instance, ondansetron (Zofran) may be prescribed every four to six hours as needed, but the insurance plan may only cover up to three doses per day. Attempting to manipulate days' supply calculations to circumvent these limits is considered fraudulent and therefore, not an option. Patients facing these restrictions are often left paying cash prices for the whole amount, sometimes exceeding $100 for just a few days' supply.

3. Non-Formulary Medications

In some cases, the insurance plan will not provide any coverage for a prescribed medication because it is not included on the plan's formulary — the list of preferred covered drugs. This often occurs with over-the-counter options such as cetirizine (Zyrtec) or certain brand-name drugs when lower-cost generics are available, such as levothyroxine (Synthroid). In these situations, the patient is responsible for the full cost unless a successful prior authorization or appeal is submitted.

4. Out-of-Network Pharmacies

Using a pharmacy outside of your insurance plan's network can result in significantly higher costs or full denial of coverage. This issue commonly arises during travel, when patients visit a chain pharmacy that is not contracted with their specific plan. "Sorry, ma'am. I know this store is a national chain, but it appears your insurance card has the wrong state silhouette on it. So your insurance is no good here."

5. Lost or Early Refills

Requests for replacement fills due to lost medication or early refills before a trip are frequently denied. Many plans strictly enforce refill timing, although some offer exceptions for travel or extenuating circumstances. When coverage is denied, patients must pay the full cash price.

Enter Prescription Discount Cards

Now that we've reviewed some common reasons behind high out-of-pocket prescription costs, the natural question is: what can patients actually do? Unfortunately, far too many simply stop taking their medications. According to the Kaiser Family Foundation, nearly half of Americans report skipping doses or failing to fill prescriptions altogether due to cost concerns. This not only leads to worsening health conditions but also drives higher overall healthcare spending through increased doctor visits and hospital admissions.

Fortunately, a growing industry has emerged to help bridge these gaps: prescription discount cards. You've likely heard of GoodRx, the most recognized name in this space. While services like GoodRx have made medications significantly more affordable for millions of patients, many people still don't fully understand how these programs work, where the prices come from, or just how much money they stand to save by utilizing these cards.

Ask most pharmacists why a cash price can suddenly drop from $75 to $20 by keying in the right discount card, and they'll likely shrug their shoulders and say: "Well, the drug companies mark them up so high that they can afford to give patients a break." While there's some truth to that, it's only part of the story.

To truly understand this market, it's helpful to look at GoodRx, which has become the dominant player. In practice, "GoodRx" has become synonymous with prescription discount cards — much like "Kleenex" or "Band-Aid." Patients frequently say "just run it on my GoodRx" even when presenting a card from SingleCare, BuzzRx, or another company. GoodRx was not the first discount card company, but it is by far the largest, commanding an estimated 80–90% of the market.

However, recent data on actual "win rates" — how often each card provides the lowest price — tells a more nuanced story. Cards such as SingleCare, BuzzRx, WellRx, Hippo, and Optum Perks can often deliver better prices than GoodRx on many medications, savings that can add up to thousands of dollars per year for patients.

GoodRx's success stems from excellent user experience, aggressive marketing, and strong partnerships with manufacturers — including favorable arrangements on high-cost drugs like Ozempic and Wegovy. While the company has earned its leading position, this article is focused on helping you, the patient, find the best possible price.

To illustrate how dramatically different cards can affect your final cost, I've included the chart below.

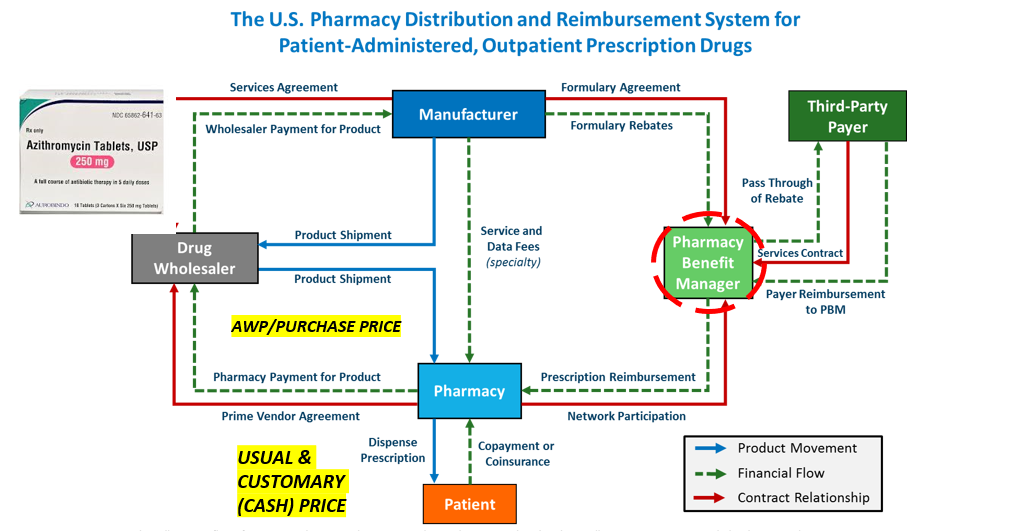

How the Pricing System Actually Works

At first glance, this chart may appear confusing or even overwhelming — and that reaction is understandable. The prescription pricing system is deliberately complex and opaque.

To keep the explanation clear and practical, let's use a common medication as an example: azithromycin, commonly known as a Z-Pak. According to DrugPatentWatch, the actual manufacturing cost for a 6-tablet course of azithromycin is less than $2. This medication is then sold by wholesalers to pharmacies for approximately $4–5 per package.

Pharmacies, however, base their "usual and customary" (U&C) cash price — the price charged to uninsured patients or used as a benchmark when negotiating with insurance companies — on the Average Wholesale Price (AWP). For a Z-Pak, this U&C price typically ranges from $30 to $45.

This raises the obvious question: how do prescription discount cards fit into this pricing structure, and how can they reduce the price so dramatically? The answer reveals much about how this system actually operates.

What gives GoodRx or any other discount card the authority to set a price? After all, if patients could simply name their own price, why not make every drug eleven cents? This question highlights how arbitrary and opaque the system can feel.

The situation reminds me of a joke by comedian Mitch Hedberg: "I think Pizza Hut has gotten too cocky with their deals. Now they're saying they'll honor any competitor's coupon. So I've decided I'm gonna open my own pizza place called Mitch's Pizza that offers free pizza for life to any guy named Mitch. We are never open."

In the same way, one might wonder: What makes prescription discount cards any different from "Mitch's Pizza"? What real authority do they have to determine what a customer ultimately pays?

Let's return to the azithromycin (Z-Pak) example. A medication that costs the pharmacy less than $5 can carry a usual and customary (U&C) cash price of $30–$45 — roughly an eight- to nine-fold markup (this is just the tip of the iceberg within the industry by the way). While part of this covers legitimate overhead costs, the markup is substantial. Importantly, insurance companies do not simply pay the full U&C amount — they negotiate.

This is precisely where prescription discount cards come in. When you use a card and pay a much lower price, the discount company has negotiated a contracted rate through Pharmacy Benefit Managers (PBMs) and pharmacy networks. These rates are lower than the cash price but still profitable for the pharmacy. Because each discount card has access to different networks and agreements, prices can vary significantly by card, pharmacy, and medication.

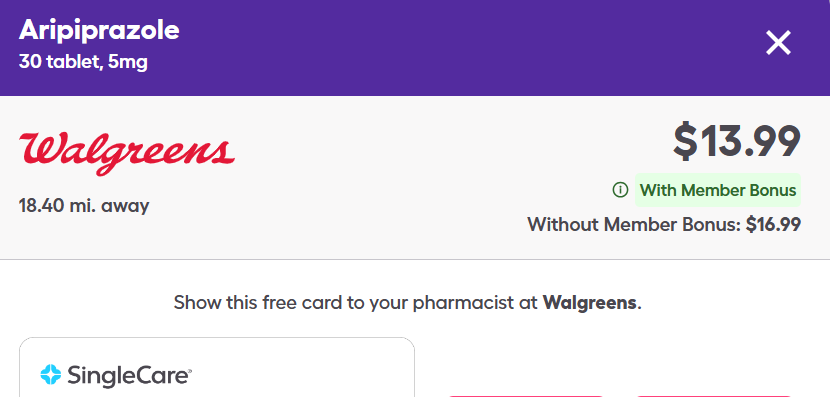

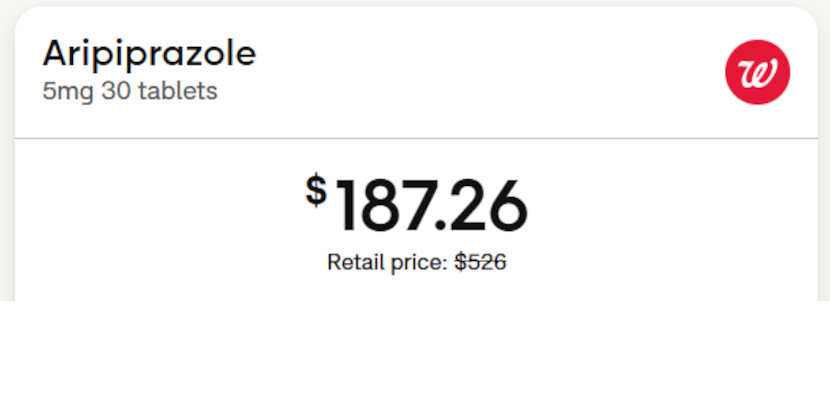

The example below shows two different discount cards — SingleCare and GoodRx — both at Walgreens, for the exact same Z-Pak on April 4, 2026. The price difference is striking, and it has nothing to do with randomness. It's the direct result of each card's unique PBM contracts and pharmacy network agreements.

Same drug. Same pharmacy. Same day. Different card — different price.

How SimpleScript Helps

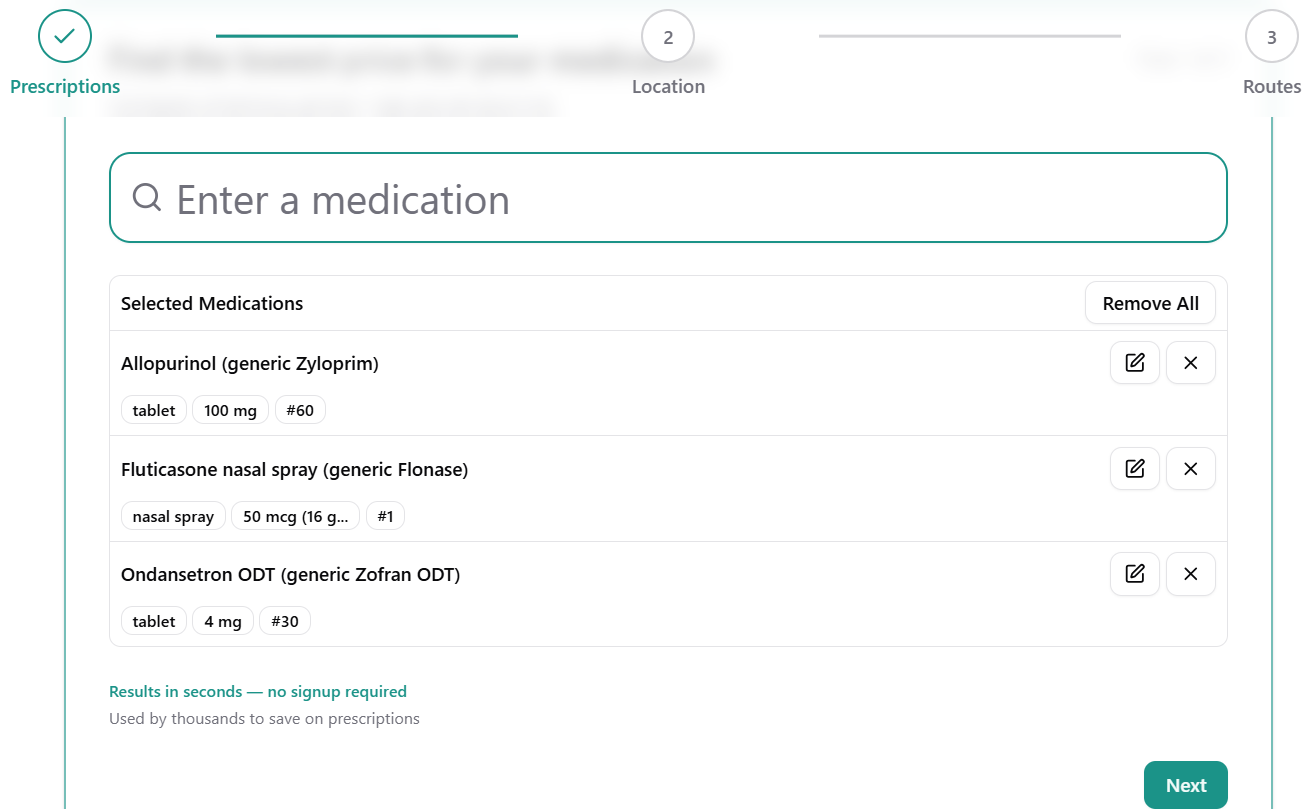

Fortunately, I'm part of the team behind SimpleScript, a company created specifically to solve this problem. Whether you've been caught off guard by a high price at the pharmacy counter, are deciding where to send a prescription, or are planning ahead to keep your household's medication costs manageable, SimpleScript removes much of the guesswork.

![]()

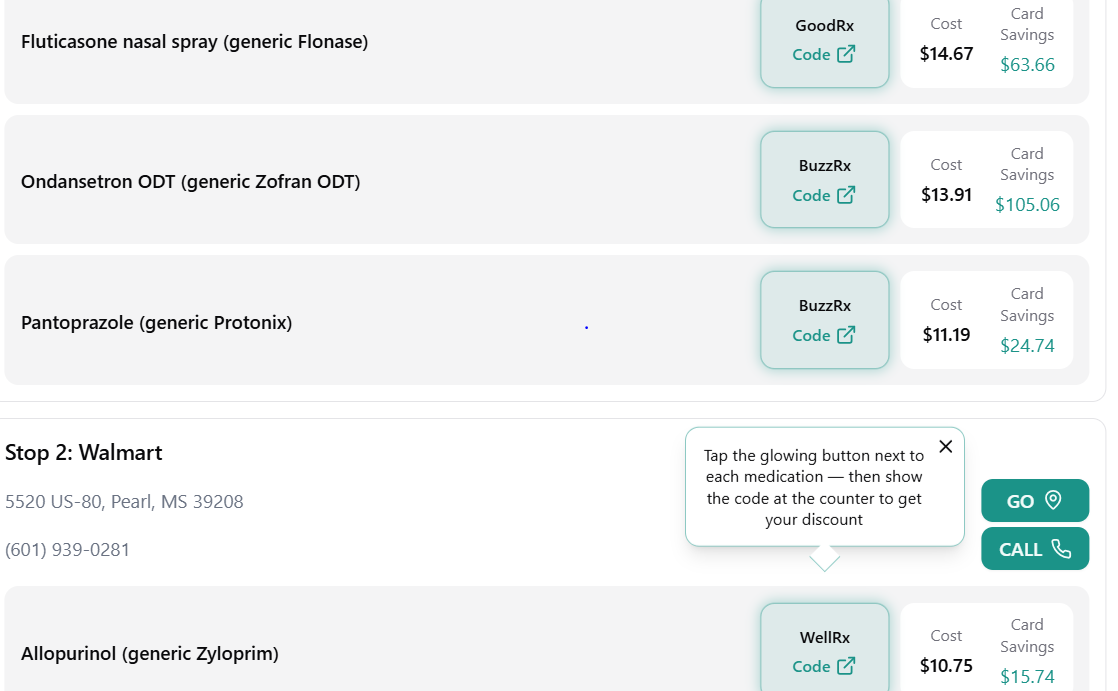

Getting started is simple: just enter your medications by brand or generic name and add them to your basket. Because SimpleScript compares multiple drugs at once, you no longer have to check dozens of different discount cards to find the best price and pharmacy for each one.

The platform also automatically flags important opportunities and alerts, including:

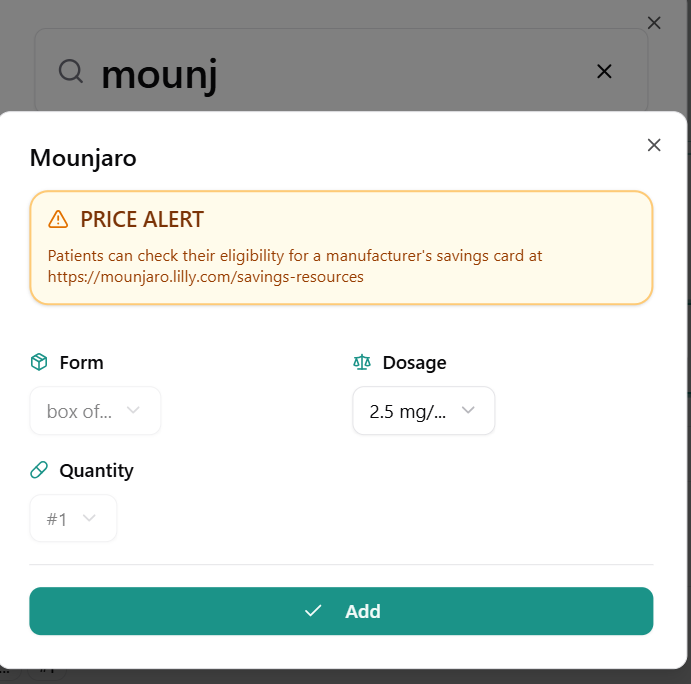

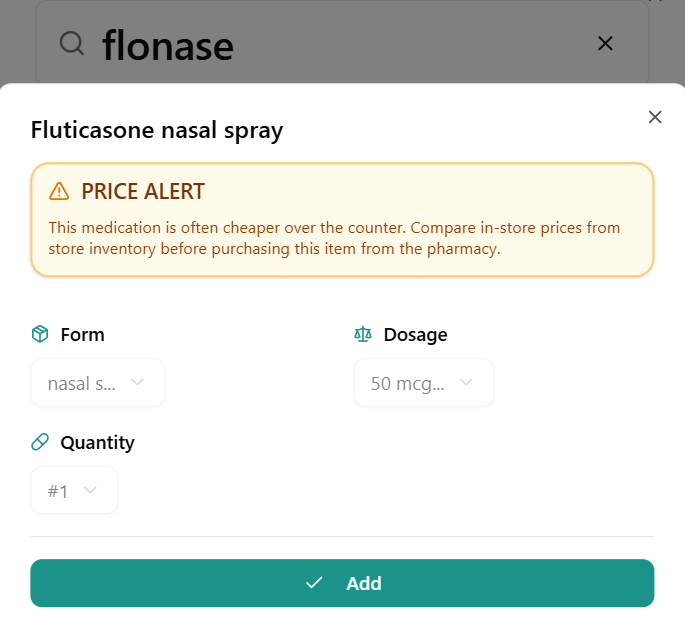

- Over-the-counter alternatives that may be cheaper than the prescription version (such as Flonase)

- More cost-effective dosing strengths (for example, allopurinol 200 mg vs. 100 mg)

- Potential drug interactions

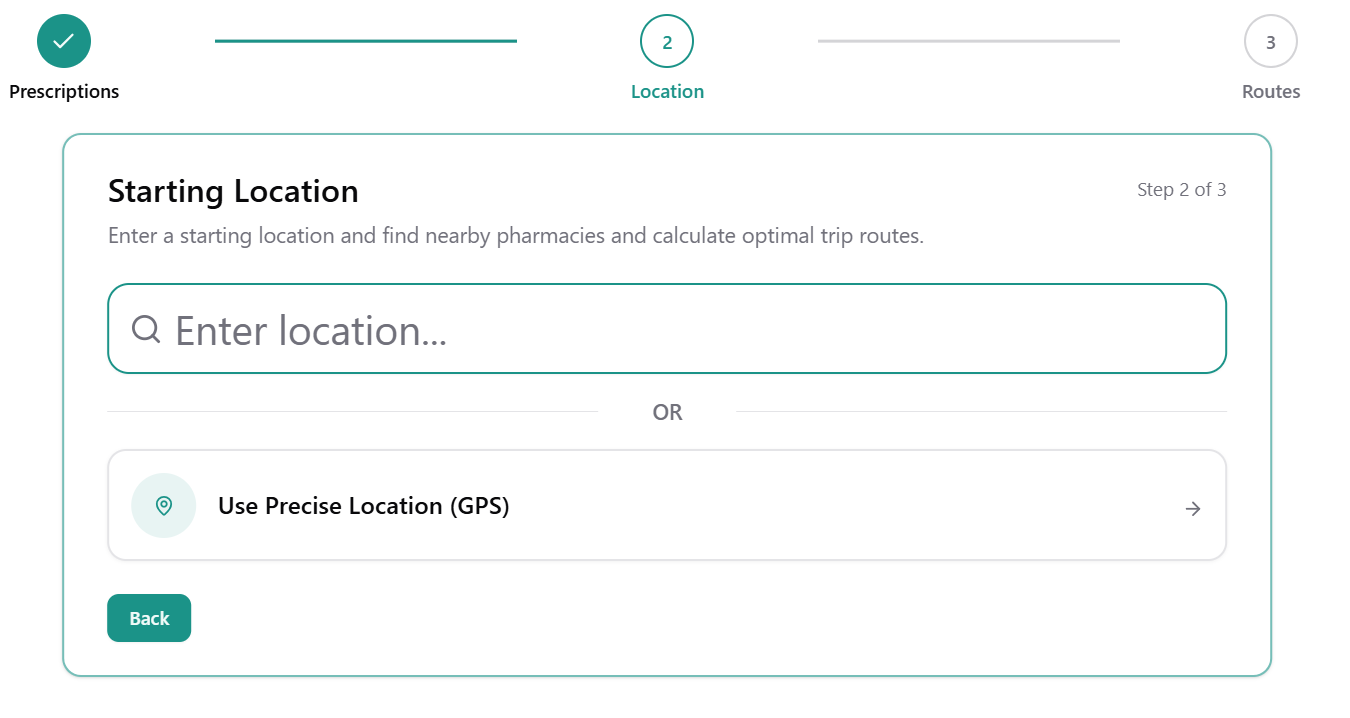

Next, enter your location — either by zip code or precise address. Our built-in drive-time optimization tool then factors in travel distance, helping you find the best balance between price and convenience. After all, driving an extra ten miles may not always be worth a small savings on your prescription.

Preferred Pharmacy Selection and an interactive map view will also be available soon.

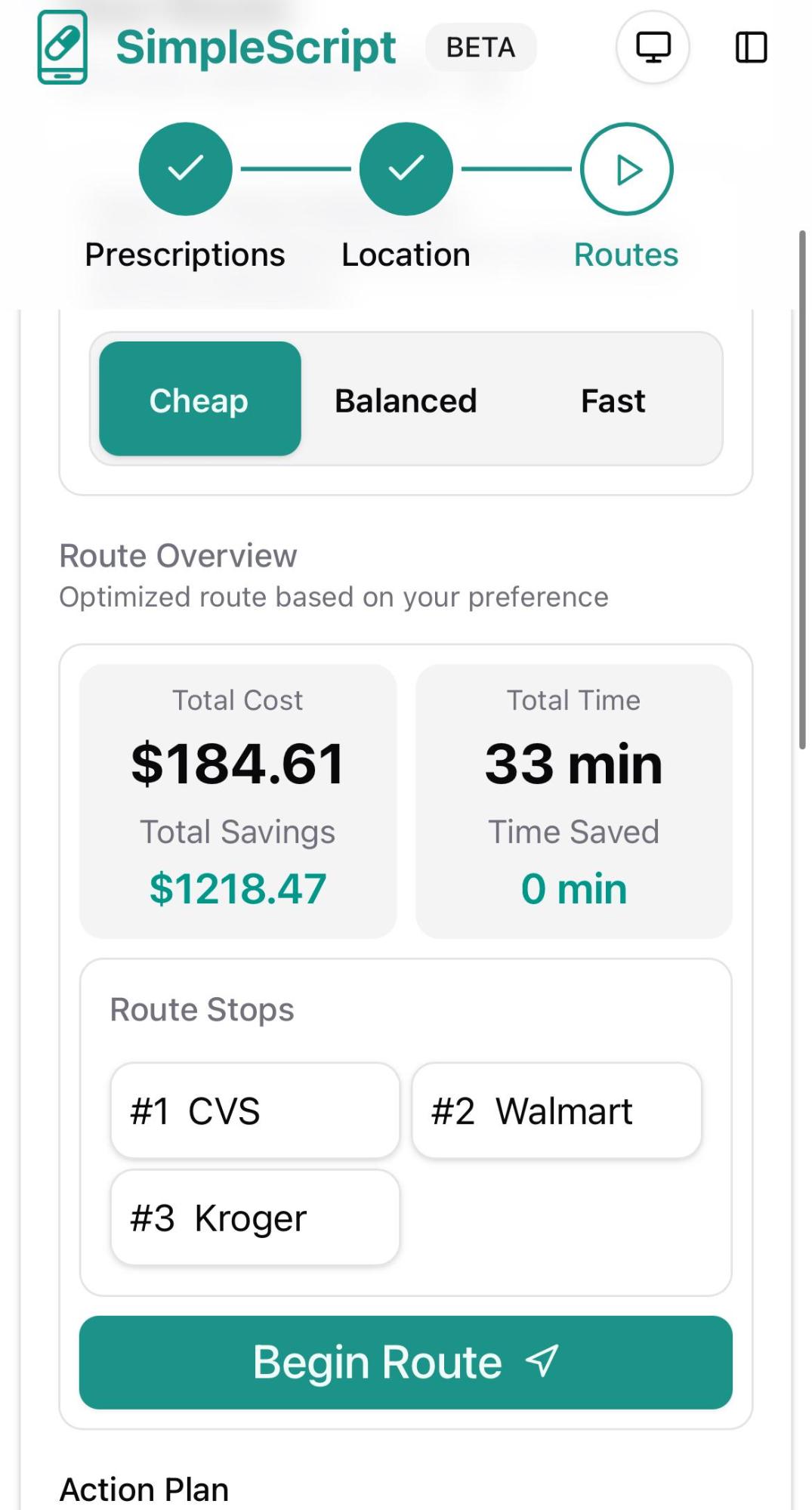

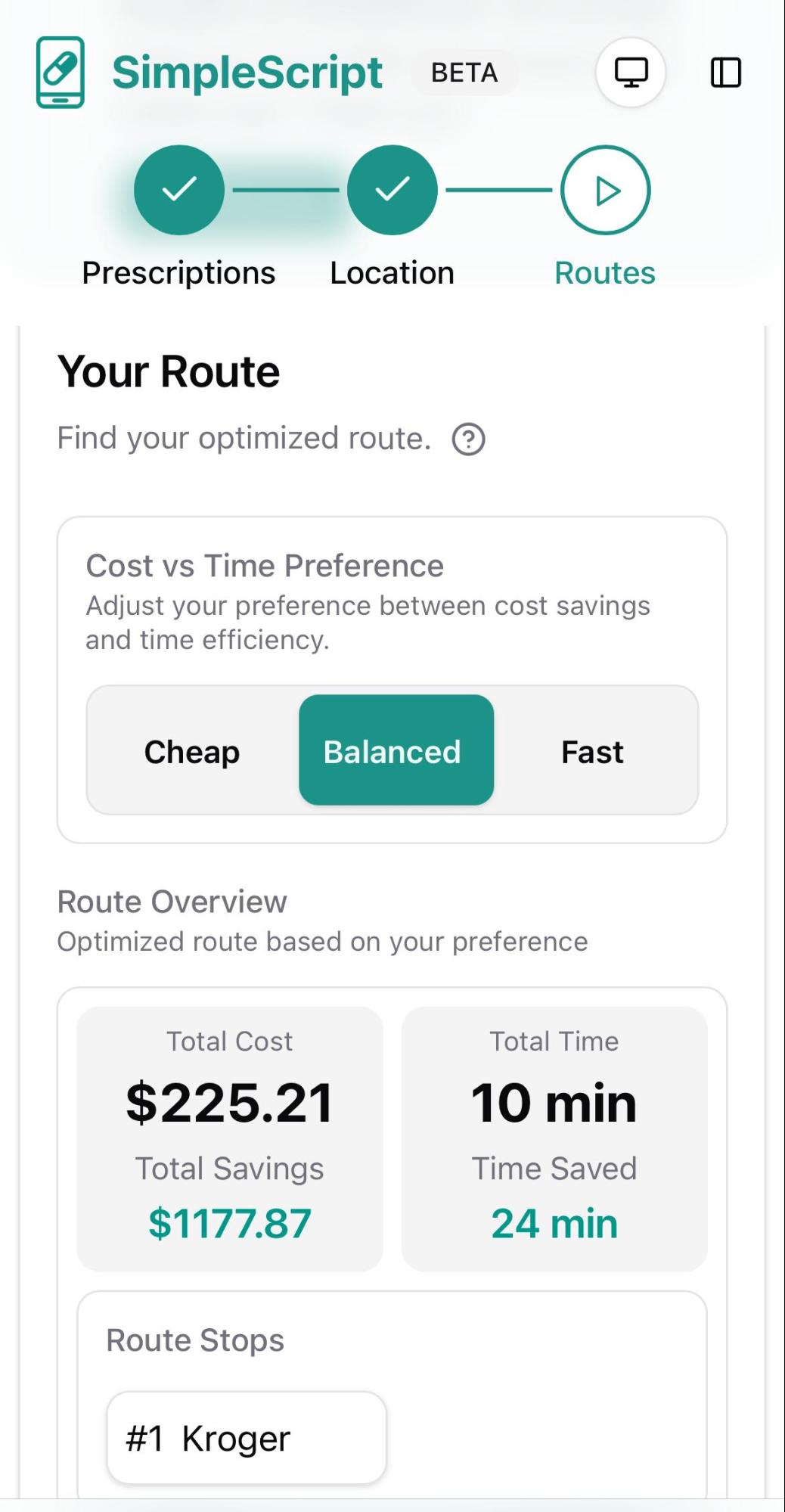

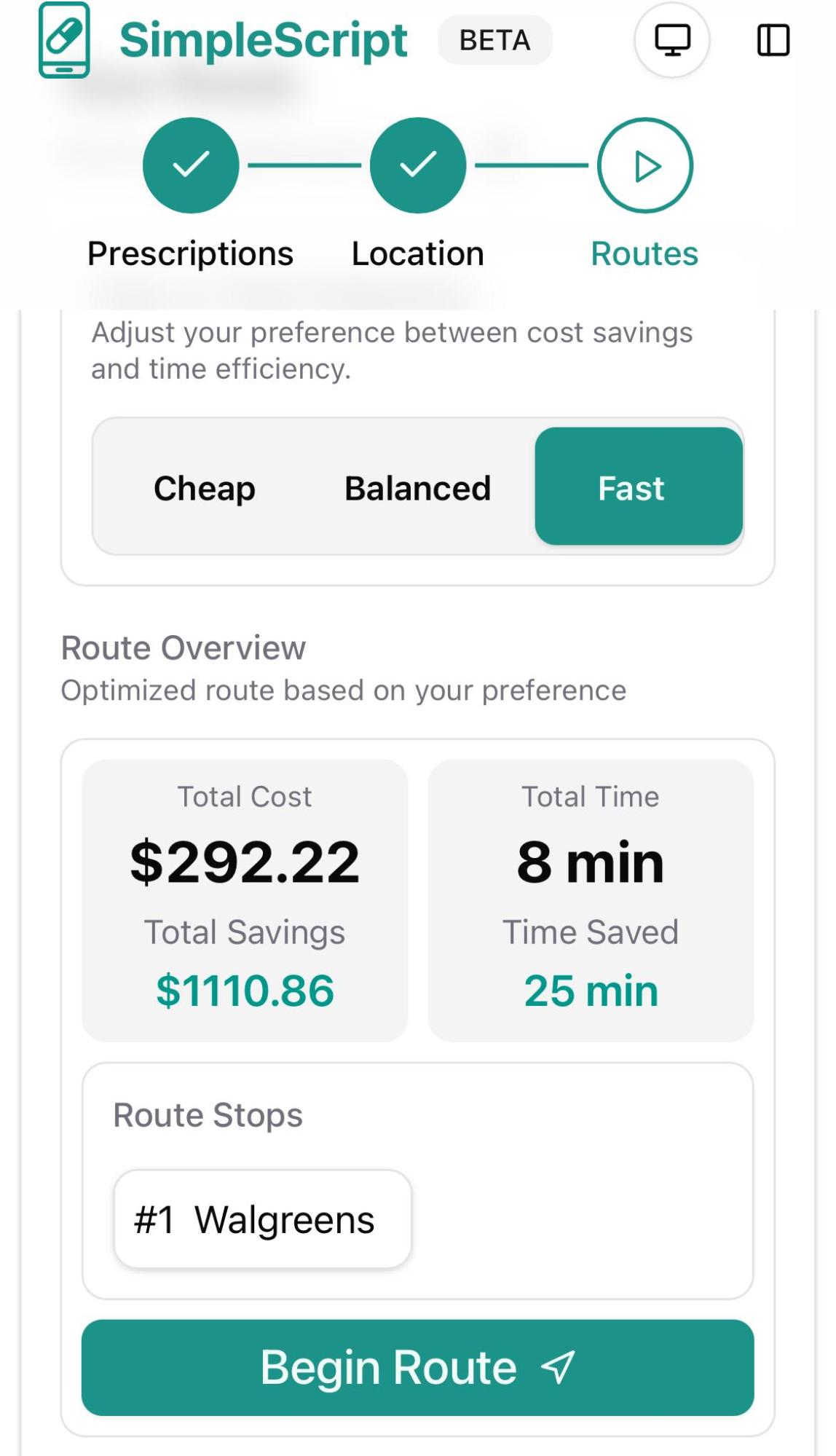

Next, you can choose from three sorting options to find the best deals according to your priorities:

- Fast: Shows the best prices available at your closest pharmacy.

- Balanced: Finds the optimal combination of low price and convenience (ideal for most people).

- Cheap: Delivers the absolute lowest prices regardless of distance or number of stops required.

As you'll see, the price differences between these options can vary significantly.

Additional filters will soon be available, allowing you to sort results by Drive-Thru Accessibility, Hours of Operation, Store Service Quality, and Mail Order Availability.

Once you've found the best option, simply select the recommended discount card. You can then present it at the pharmacy (or use the provided details) to redeem your discounted price.

Whether or not you use SimpleScript, I'm genuinely glad to help shed light on this complex and under-understood subject. My hope is that the information shared here helps you save money, reclaim your time, and protect your long-term health.

Thank you for reading.